The African Colo Gold Rush

African data center colocation market growth has hit an inflection point. After 3-4 years of solid, if unspectacular growth, the region’s available capacity is exploding, seemingly impervious to a context of extreme economic stress. Full-stack cloud data centers have arrived, IXP and CDN rollout is accelerating and enterprises are externalizing their workloads to colo facilities.

The African data center sector is riding a wave of deep-seated, pandemic-boosted structural transformation of the digital workplace and enterprise IT architectures – it is, unquestionably, one of the few winners in Africa’s COVID-19 new normal.

It is often said that revolutions need seminal shocks that catalyze participants into transformative action. And so it is for the African data center space, which has essentially witnessed three such groundbreaking moments over the past three years. The 2017 announcement by Microsoft that it would be offering its Azure cloud services directly from Africa-based data centers; the second catalytic event was the South African power crisis of late 2019 helped convince undecided large corporate customers of the economic and practical incongruity of managing complex non-core IT assets. And then there was the COVID-19 pandemic which further underscored the need for enterprises to transform their IT architectures to adapt to a complex office-less, everywhere, any-time, by everyone access to critical enterprise workloads.

These market shocks have accelerated the maturation of this industry, from a smattering of small, substandard facilities to what is now, in effect, one of the fastest-growing colo markets in the world.

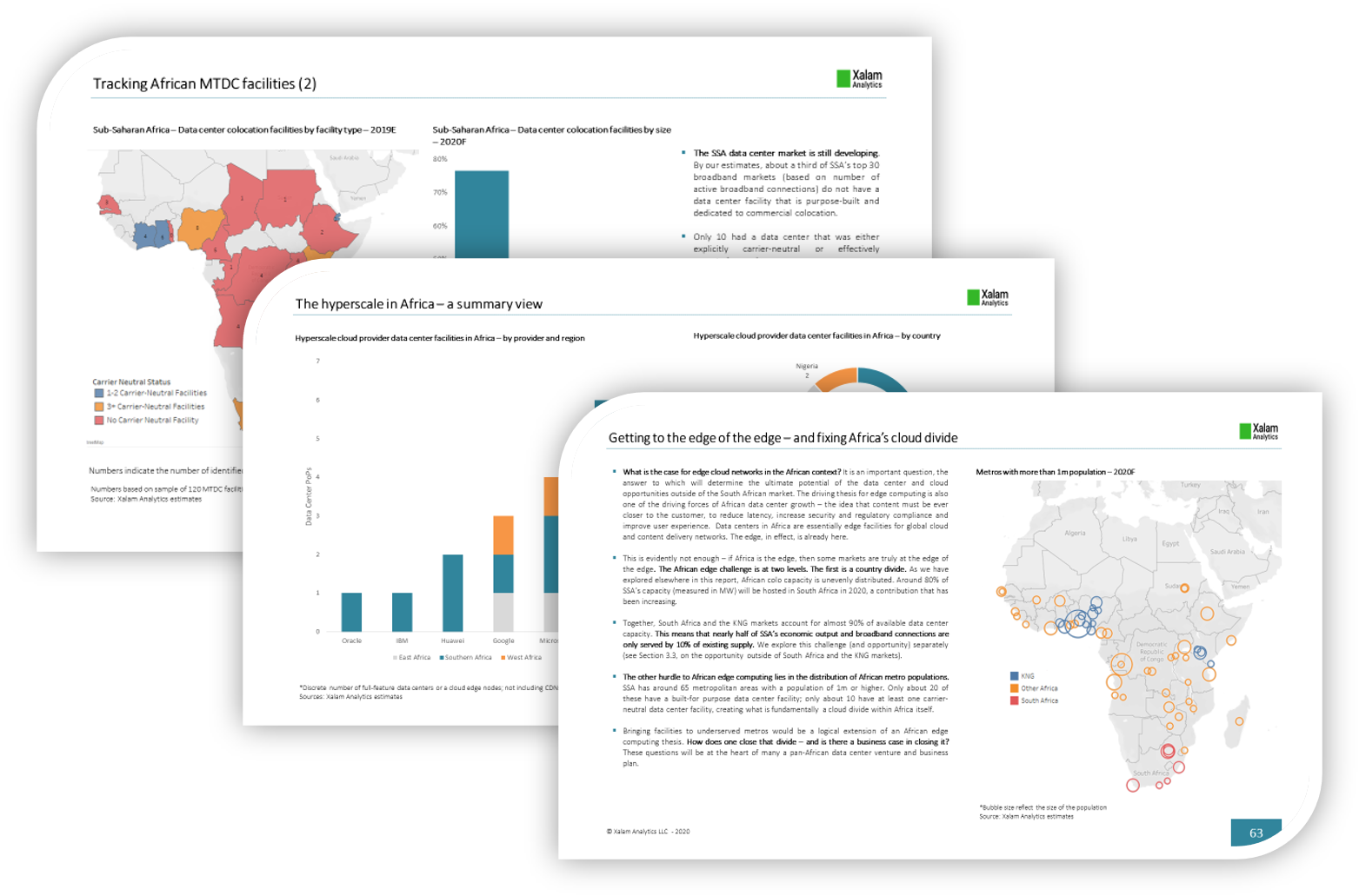

The African Data Center Gold Rush is our most comprehensive research to date on the data center colocation market in Sub-Saharan Africa (SSA), leveraging months of research and interviews, extensive data collection and new analytical tools for data center analysis and geo-mapping. The report provides an unprecedented view into the dynamics underpinning the SSA Multi-tenant Data Center colocation market – all with the Xalam team’s uncompromising focus on finding investor value – wherever it may be. Among key findings, the report provides a data-driven exploration of the following key areas:

-The size, nature and evolution of the SSA MTDC colocation market;

-Why this sector seems so impervious to the COVID-19 induced economic devastation surrounding it;

-What the growth outlook looks like for SSA’s largest colocation markets: South Africa, Kenya, Nigeria and Ghana;

-Whether South Africa is at risk of getting oversupplied;

-Where the best SSA data center colocation opportunities lie, outside of South Africa and the KNG markets;

-How African colocation providers manage the continent’s challenging power infrastructure, integrate renewable sources of power – and what that means for their ability to scale;

-From colo MRR to CapEx per rack, the evolution of SSA’s key data center business metrics;

-Where the hyperscale providers are likely to go next, now that they have full-stack data center facilities in South Africa;

…and more.

A reference report for all players and investors in African digital infrastructure and cloud markets.